Bank economists expect credit conditions to continue improving for both consumers and businesses over the next six months, according to the American Bankers Association’s latest Credit Conditions Index released on Jan. 25.

The latest summary of ABA’s Credit Conditions Index examines a suite of indices derived from the quarterly outlook for credit markets produced by ABA’s Economic Advisory Committee (EAC), which is comprised of chief economists from major banking institutions across North America. Readings above 50 indicate that, on net, the economists expect business and household credit conditions to improve, while readings below 50 indicate an expected deterioration.

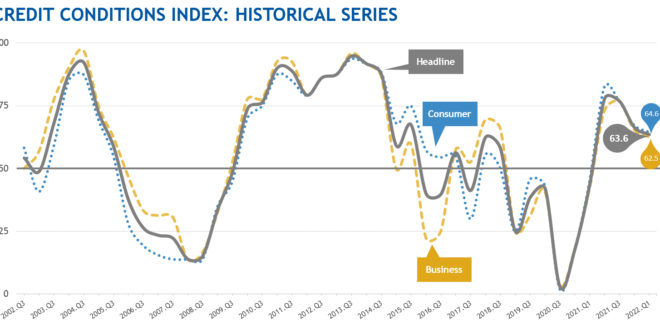

The first quarter 2022 report finds that near-term expectations for credit quality and availability eased modestly for consumers and businesses in January after a more pronounced decline in October. Despite the downward movement, the index suggests that credit quality and availability is expected to improve over the next six months. As the economy continues to normalize, the anticipated pace of improvement is expected to slow relative to the rapid recovery experienced in preceding quarters.

“Inflationary pressures, the Omicron surge, continuing supply chain constraints and expectations for higher interest rates have clouded the near-term economic outlook,” said ABA Chief Economist and Head of Research Sayee Srinivasan. “However, overall credit conditions remain sound, and both consumers and businesses are well-positioned to drive economic growth this year.”

In the first quarter of 2022:

- The Headline Credit Index slid 2.7 points to 63.6 in Q1 following a larger decline in Q4. While the current reading is the lowest in a year, it is still well above 50, signaling that bank economists expect credit market conditions to improve over the next six months.

- The Consumer Credit Index also decreased 2.7 points to 64.6 in Q1 but continues to signal improving credit market conditions. Half of EAC members expect to see consumer credit availability improve over the next two quarters, while none expect it to deteriorate. Meanwhile, the expectation of increased consumer access to credit has not sparked concerns of eroding credit quality; 83% of EAC members expect consumer credit quality to hold steady or improve over the next six months.

- The Business Credit Index declined 2.9 points to 62.5 in Q1 but remains elevated. As with consumer credit, half of EAC members expect business credit availability to improve over the next two quarters while the others expect conditions to remain unchanged. Meanwhile, most EAC members expect little change in business credit quality, and the others are split evenly between improvement and deterioration.

The full report with detailed charts and a discussion of the broader economic context is available here.